In terms of our common law, any person with full legal capacity may enter into contracts in South Africa unhindered, and this is actually done on a daily basis - be it the foreign tourist who books accommodation or a flight, or purchases a souvenir, a car or a property, or an off-shore company wishing to conduct business in South Africa and entering into a contract for the purchase of South African goods.

If you receive an offer to purchase from a foreigner (i.e. non-resident) you may use your standard sale agreement and generally speaking, the agreement will be as binding as any contract concluded between two South African residents provided the non-resident had full legal capacity to conclude such contract.

Legal Capacity to enter into a sale agreement for land

The only difference in relation to property transfers is the provisions of the Matrimonial Property Act which determines the legal capacity of parties married in or out of community to enter into contracts for the sale of land.

For example, in terms of South African law, a minor, that is a person under the age of 18, would have to be assisted by his or her legal guardian in order to conclude a valid contract, and parties married in community of property will not be able to purchase property without the assistance of the other spouse in terms of the provisions of the Matrimonial Property Act.

Our Matrimonial Property Act does not however apply in respect of foreign marriages and the legal regime that determines the legal capacity of such person to conclude a contract for the sale of land, is determined by the laws of the country where such person was domiciled (living) at the time of the marriage.

The law of such other country will determine if such foreigner has the necessary legal capacity to enter into a contract for the purchase and sale of land in South Africa with or without the assistance of their spouse.

In terms of say Zimbabwean law, parties are generally able to conclude agreements for the purchase of land without the assistance of the other spouse and the same applies in respect of marriages concluded in the United Kingdom.

However, our courts and our Deeds Office cannot take cognisance of or apply foreign law as they would South African law.

The Deeds Office will thus not accept documentation signed by a person who was married in terms of foreign law unless the spouse of that person has consented to such sale and/or is a party to that transaction.

This means that you may have a perfectly valid sale agreement (depending on the marital status of the signatories in terms of their country of origin) but be unable to enforce it.

DEEDS OFFICE REQUIREMENTS IN ORDER TO EFFECT TRANSFER

A valid contract of sale does not in itself confer ownership of land, nor does it provide security for payment of a bond - transfer of ownership pursuant to a valid sale must take place in the Deeds Office.

In terms of our Deeds Office regulations, the Deeds Office requires both spouses to sign all transfer documents in order to pass ownership - regardless of whether or not the sale agreement required the signature of only one or both spouses.

The Deeds Office will not take cognisance of the provisions of foreign law and many sales come unstuck by virtue of this provision where for example, spouses are estranged and cannot be contacted.

The only way around it would be a declaration from the Embassy of such country setting out and confirming that the spouse would not require the assistance of the other spouse.

The transferring attorney's requirements in order to effect transfer would be similar to that of a transfer to a South African resident, except that both spouses would have to sign the conveyancing documentation.

The following documents would be required:

- a certified copy of the Purchasers’ passport;

- a certified copy of their work permit and temporary residency (if applicable);

- a certified copy of proof of residence and South African income tax number (only if applicable).

Estate agents should thus ensure that sale agreements are signed by both spouses in the event of a foreign marriage - this applies regardless of whether or not the person is a resident or non-resident.

Advice:

Make enquiries with your foreign buyer and establish up front if you are going to run into any problems - if so, your foreign buyer can purchase the property through a South African registered company in which event spousal consent would not be required.

FINANCING THE TRANSACTION

South African exchange control regulations determine the extent to which non-residents can borrow money locally to fund the purchase.

Non-resident purchaser who does not work in South Africa

A non-resident purchaser will not be allowed to borrow more than 50% of the purchase price to fund the purchase. The balance must be paid in cash and this may be cash generated in South Africa, or off shore funding.

Non-resident purchaser who is on a termporary work permit in South Africa

A person working in South Africa, and who has a temporary work permit, may borrow more than 50% of the purchase price, and the amount of the loan will depend on the bank’s criteria. A condition of the loan will however be that the purchaser reduces the bond to less than 50% of the registered amount before they return abroad.

Some banks may require a work permit of at least 4 years before they would consider a bond for more than 50% of the purchase price.

The banks generally will require the following documentation to consider a non-resident for bond approval:

- a certified copy of the passport;

- 3 months overseas bank statements;

- 3 months payslips (6 months statements and payslips where the Purchaser earns Commission or is paid overtime).

INVESTMENT OF FUNDS IN CONVEYANCERS TRUST ACCOUNT PENDING TRANSFER

Foreign Exchange and Banking regulations have now been amended with regard to the investments of funds for non-residents pending transfer. Conveyancers are no longer able to invest money in a Sec78(2A) account to earn interest for the benefit of the non-resident purchaser and such investments can only be made for people with SA identity documents.

This must be taken into consideration and the standard clause dealing with the investment of the deposit in an interest-bearing account for the benefit of a purchaser must be deleted - the funds will simply be held in trust pending transfer, with no interest accruing to the non-resident purchaser.

INTRODUCTION AND REPATRIATION OF FUNDS

Once a foreigner has introduced cash into the country with a view to purchasing a property, he can repatriate it (together with the profits thereon) provided he has brought the funds through the proper channels when it was first introduced to the country.

The following documentation should be retained by such non-resident purchaser to avoid delays with the repatriation of the funds on resale:

- proper proof must be kept by the foreign purchaser of the origin of the purchasing funds, including statements on the foreign transferring account as well as the receiving conveyancer’s bank statements;

- a copy of the original sale agreement.

Upon the eventual onward sale of the property, application will be made for Exchange Control Approval for the repatriation of the funds, supported by the following documents in addition to the documents as set out above:

- sale agreement (onward sale);

- conveyancers final statement of account reflecting calculation of the sale proceeds;

- foreign bank account information;

- ID and proof of residence of non-resident.

SIGNING OF CONVEYANCING DOCUMENTATION OUTSIDE THE COUNTRY

Conveyancing documents must be signed before either a notary public of the country where the person resides, or at the South African Consulate or Embassy in such country.

This can be a time consuming and expensive exercise which is governed in terms of international law. (The Hague Convention).

It is cheaper to sign such documents with the South African Embassy in say London but an appointments needs to be made to do so and this can take up valuable time.

An onerous title deed condition that isn’t discovered in time could delay or prevent the progress of a property development – with serious cost implications. Alternatively, such an omission could be costly when buying or selling property.

Given this truism, the purpose of this article is to sensitise the reader to some pitfalls when dealing with title deeds.

The deeds registration offices had a system whereby deeds were lodged in duplicate and the Deeds Office would endorse changes of ownership, caveats, interdicts, mortgage bonds, and servitudes against the title deeds. They would keep one copy for records purposes and the other copy would be given back to the client.

It was not practice, nor prescribed in any Act, that conditions be carried forward from deed to deed. In the Deeds Registries in the former Cape Province the so-called pivot deed system had existed prior to 1937. The pivot deed system is unique to the Cape Town deeds registry. In terms of this system, no conditions were carried forward in a title deed. The title deed conditions would simply state:

“Subject to the conditions as contained in Deed of Transfer No … [with reference to the prior

title deed]”.

When searching the above pivot deed, one would find that these deeds in turn make reference to earlier title deeds.

It is only since 1937 that title deed conditions have been carried forward in each new title deed. Thus, to determine all the possible conditions against and in favour of a property, proper research must be done and all previous title deeds must be checked, from the day when the first Government Grant or Crown Grant was issued up to 1937.

The practical way would be to employ a conveyancing attorney, skilled in these matters, to conduct the research and prepare a Conveyancer’s Certificate to certify that

* the Conveyancer did a search behind the pivot deed and

* found no onerous conditions relevant to the proposed nature of the transaction or development, etc.

Developments since the 1980s

The Deeds Registration offices introduced a micro filming system, and since then all title deeds lodged are microfilmed. In addition, a scanning system was introduced in 2007/ 2008. Thus, Deeds Office records are now kept on both microfilm and in digital format, while the original title deeds are sent back to the attorneys for delivery to the new owner or bank(s). Title deeds are endorsed with changes in ownership, mortgage bonds and all other propertyrelated transactions. This of course depends on the instruction the deeds office had received on lodgement from the conveyancing firm.

The Deeds Offices continually update their records and one can obtain a “Deeds Office printout” to view the most current information listed against the property, viz.:

- Interdicts and caveats (examples are court orders, insolvency and rehabilitation notices, sequestration orders, liquidation orders, notices from the Surveyor General’s office, and expropriation notices).

- Sectional title information, such as

- Exclusive use areas.

- Rights of further extension reserved by the developer (section 25).

- Servitudes on common property.

- Notarial servitudes

- Mortgage bonds

It is, however, also important to note that updated information pertaining to property transactions can take, from date of registration, as long as 5-8 working days to appear on the system of the Deeds Offices. Sectional-title transactions can take up to 10 days and other transactions that involve cross-writing in title deeds filed in counter cover can take up to three weeks.

(Cross-writing is the updating of all relevant and related information in documents filed at Deeds Registration offices. The counter-cover system applies where 20 or more properties are held under one title deed, and where the client requests the Deeds Office to keep the original title deed in its records.)

Some advice

In sum, to protect one’s interests, it is a good idea to appoint a conveyancing attorney to conduct a search at the Deeds Office and peruse or verify the following information that might be applicable to the subject property:

- Conditions in the current title deed

- Conditions behind the pivot deed

- Information on the Deeds Office printouts, such as:

- Caveats.

Servitudes.

Interdicts.

And, lastly, if you are a developer, remember to appoint a town planner to assist with the restrictions imposed by the local authority and, if applicable, zoning requirements.

Having bought his dream home, Harry felt sure that his investment was secured against all unforeseen mishaps. After all, he had taken out home owners insurance with one of the leading insurance companies, according to the conditions of his bond approval. He could now happily begin paying the bond instalments.

Everything went well for a year or two, until Harry decided it was time to extend the home by adding another bedroom. He had the plans drawn up by a friend of his, a respected local architect, but great (and unpleasant) was his surprise when he tried to lodge his plans at the municipality. Here they told him that some of the existing improvements on his property were in fact illegal. Upon further enquiry, it was determined that the previous owner had constructed the indoor braai area without approved plans. As a result, the municipality refused to approve his new plans and, to his horror, he discovered that his home owner’s insurance policy specifically excludes any structures not approved by the local authority AT THE TIME OF CONSTRUCTION. That meant that, even if he obtained the municipality’s approval afterwards, the indoor braai area would not be covered by the policy. When Harry complained that the municipality had given a rates clearance on the property before it was transferred into his name, the municipal official just shrugged.

Harry’s only recourse now was to approach the previous owner, who may or may not defend any action against him and who may or may not have sufficient funds, should Harry suffer any damages pertaining to the braai room. What happens if there is a leak and the rest of the house is flooded? Who will pay if the walls collapse and damage occurs to the rest of the house? Worse still, is that Harry would be obliged to disclose this information to a prospective purchaser, should he decide to sell the house.

The best solution to this kind of problem is, unfortunately, no longer available to Harry, namely “prevention is better than cure”.

So, when buying a home, make sure that the entire construction has approved building plans and know what:

• is included and excluded in your home owners insurance policy; and

• what your obligations are.

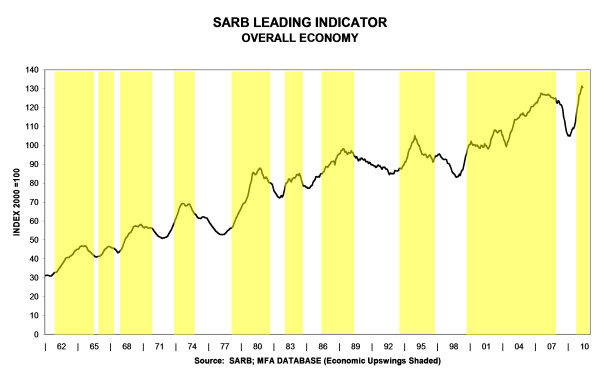

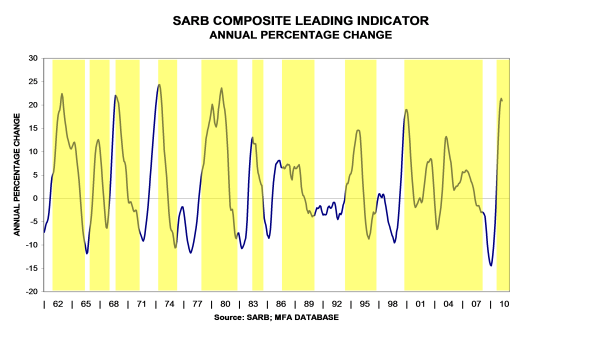

SARB Leading Indicator, Vehicle Sales, Transfer Duty & House Prices

The SARB leading indicator dropped marginally, possibly reflecting some moderation in the economic growth rate …

… yet, the annual percentage increase is very high because of comparative base effects (i.e. current levels are being compared to very low levels a year ago)

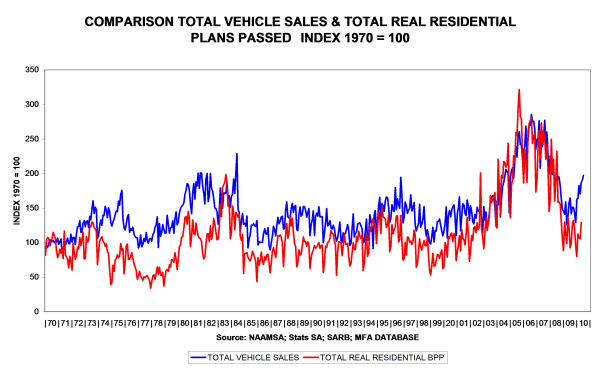

Vehicle sales have benefited from World Cup purchases and comparative base effects … the time series plans passed is forming a trough.

In percentage change terms, vehicle sales are performing well (+23% year-on-year), partly because of comparative base effects. In the near future this leading indicator is expected to moderate as higher current levels will be compared to higher levels a year ago

The trend in the residential property market is still upward …

… yet, in real terms, the revival is not as robust as was the case in 1999 because mortgage finance is currently scarce

In percentage change terms the rise is conforming to pattern. Note that early in the upswing phase of the business cycle the growth rate is robust, but as can be seen in the circled areas, after a while it tapers off.

Nominal house price increases are taking a breather

Real house prices are still below their peak levels in 2007

Even though the time series Transfer Duty Paid is more volatile than House Prices, they seem to reflect similar trends – currently positive, but both moving sideways

The implementation of the Consumer Protection Act has been postponed to the 1st of April 2011 as the Minister of Trade and Industry is still in the process of finalising the regulations to the Act. They are also putting in place the structures required to implement the Act, namely the Consumer Commission and the Consumer Tribunal which will deal with complaints and disputes.

The Consumer Protection Act brings about a fundamental change to our common law which up to now has regulated contracts concluded between suppliers and consumers. It also deals with the protection of consumers in general.

It has created basic 'Consumer Rights' - such as the right not to be discriminated against on the basis of for example sex or race in the conclusion of contracts, and outlaws 'unconscionable conduct' on the part of a supplier of goods or services and protects consumers against unfair or misleading marketing practices.

Estate agents will be well advised to familiarise themselves with the provisions of the Act as they will now also have a legal duty of care towards buyers in addition to their duty in terms their mandate to their sellers.

In terms of the Consumer Protection Act, an estate agent must ensure that his or her marketing of a product (i.e. the property to be sold) ties up with the actual nature and quality of the property that is sold. The days of 'Sales Talk' is over and if an agent is aware of a defect or potential problem with a property, they would be duty bound to bring this to the attention of the buyer, failing which they may face a claim against their agency by virtue of their false or misleading conduct.

By way of example, if an estate agent makes a statement to the effect that a property is zoned commercial when this is not the case, and if this has a material effect on the value of the property purchased, the buyer may well in terms of the CPA have grounds to claim the difference between the purchase price paid and the actual market value of the property from the agent.

It is thus critical that estate agents make themselves fully acquainted with the nature and extent of a property, and of defects which are reasonably foreseeable before they take a property on their books. It may also be a good idea to obtain an indemnity from a seller to protect the agent against sellers who may not have made a full disclosure to them at the time that the property is listed with the agency and the mandate is signed.

Estate agents should also review their mandates with sellers to make sure the terms thereof are just and fair, if not, they may have difficulty enforcing commission claims.

GEUE v VAN DER LITH (20 NOVEMBER 2003)

APPÈLHOF SAAK: 625/02

1. Die Appèlhof het op 20 November 2003 beslis dat die vereiste gestel in Art. 3(e)(i) van die Wet op die Onderverdeling van Landbougrond (Wet 70 van 1970), naamlik: dat geen deel van landbougrond sonder die Minister van Landbou se toestemming verkoop mag word nie, ʼn absolute vereiste daarstel. Dit beteken dat ʼn kontrak vir die verkoop van ʼn deel van landbougrond nietig is, al word dit opgeskort hangende die Minister se toestemming.

2. In casu het Van Der Lith ʼn deel van sy plaas Cantebury in Limpopo aan die egpaar Geue verkoop. Die kooptransaksie was onderworpe aan ʼn opskortende voorwaarde dat die Minister van Landbou moet toestem tot die beoogde onderverdeling alvorens die koop bindend is. Die Minister se toestemming is inderdaad later verkry toe die egpaar weens ongenoemde rede in die Hooggeregshof in Pretoria vir die nietig verklaring van die kontrak gevra het omdat dit nie aan die vereistes van Art. 3(e)(i) voldoen het nie. Die Hooggeregshof het bevind dat die kontrak nie nietig is nie. Die Appèlhof het beslis dat die kontrak wel nietig is, aangesien dit nie aan die vereistes van Art. 3(e)(i) voldoen het nie. Art 3(e)(i) is ʼn absolute vereiste.

3.1. Die beslissing bevestig dat ʼn kooptransaksie van ʼn deel van landbougrond nietig is, indien die Minister van Landbou se toestemming nie vooraf bekom is nie.

3.2. Die beslissing bevestig verder dat ʼn kontrak vir die verkoop van ʼn deel van landbougrond nietig is, al word dit opgeskort hangende die Minister se toestemming.

4. PRAKTYK NOTA

4.1. Dit is dus raadsaam om die nodige toestemming tot onderverdeling te bekom alvorens u ʼn kontak vir die koop van ʼn deel van landbougrond opstel. U kan professioneel aanspreeklik gehou word vir skade gelei deur die teenkant in ʼn geding indien die verkoper of die koper weens ongenoemde rede vir die nietig verklaring van die kontrak vra omdat dit nie aan die vereistes van Art. 3(e)(i) voldoen het nie.

The Minister of Trade and Industry, Dr. Rob Davies, has deferred the general implementation date to 1 April 2011.

The postponement will give business and the public sufficient time to prepare them for compliance with the new law.

However, the regulations are still outstanding and it is difficult to get a full picture of the impact.

The public and stakeholders can approach the National Consumer Commission for assistance and guidance as soon as their establishment is announced, which is expected in the third quarter of this financial year.

The act focuses on the protection of the consumer to “promote a fair accessible and sustainable marketplace for consumer products and services and, for that purpose, to establish national norms and standards relating to consumer protection.”

The act is the result of the intention of the Department of Trade and Industry to “create and promote an economic environment that supports and strengthens a culture of consumer rights and responsibilities.”

It seems at this stage that the act only applies to transactions that are concluded in the ordinary course of the supplier’s business. Therefore it would for instance apply to property sold by a developer and to the services provided by estate agents to sellers, but not to once-off transactions between buyers and sellers of property.

Therefore, developers, speculators and institutional investors with large property portfolios who sell property in their ordinary course of business, cannot exclude their liability for defects by way of a voetstoots clause.