Jou strandhuis is in die mark vir verkoop of verhuring. Die Franse paartjie het die advertensie op die internet gesien, kontak gemaak uit Frankryk en stel belang om jou strandhuis te koop of te huur vir vakansies in Suid-Afrika of selfs later in te woon indien die man se aanstelling as streeksbestuurder van die nuwe Afrika-been van sy Franse maatskappy realiseer. Is dit so maklik? Kan jy sommer net jou huis so oor die telefoon verhuur of verkoop aan hierdie buitelanders? Sal die transaksie geldig wees en is daar spesifieke vereistes vir so ‘n transaksie? Die antwoorde op hierdie vrae is van groot belang vir verhuurders en verkopers wat buitelandse huurders of kopers in gedagte het.

In kort, die antwoord is ‘ja’ dit kan so maklik wees. Buitelanders se eiendomstransaksies is onderhewig aan dieselfde wetgewing en regulasies as Suid-Afrikaners se eiendomstransaksies. ‘n Buitelander het dus nie nodig om fisies in Suid-Afrika teenwoordig te wees om jou strandhuis te huur of te koop nie.

Die koopprys van die eiendom kan deur die Franse paartjie in geheel met buitelandse fondse betaal word en is die enigste vereiste dat die buitelandse fondse in ‘n genomineerde Suid-Afrikaanse bankrekening inbetaal moet word. Hierdie bankrekening sal gewoonlik die trustrekening van die plaaslike oordragsprokureurs wees. Waar ‘n buitelander egter by ‘n plaaslike finansiële instelling finansiering wil aangaan vir die koop, is daar wel ‘n beperking dat slegs 50% van die totale koopprys by ’n Suid-Afrikaanse finansiële instelling geleen mag word.

Verder, indien die Franse paartjie die oordragsdokumente en verbanddokumente in Frankryk wil onderteken (buite die grense van Suid-Afrika) vereis ons reg dat die dokumente voor ‘n notaris van daardie land geteken moet word en dat die notaris se amp bevestig moet word deur die betrokke land se howe. Hierdie kan ‘n tydrowende proses wees waar die buitelanders nie by magte is om die dokumente in Suid-Afrika te kan onderteken nie. Hierdie addisionele vereistes is nie van toepassing op ‘n huurooreenkoms nie, omdat die ooreenkoms nie by die Aktekantoor registreer moet word nie.

Waar die Fransman se aanstelling later realiseer en hulle besluit om in jou strandhuis te woon, sal die paartjie se wettige verblyf hier onderworpe wees aan die Immigrasie Wet wat beteken dat hulle ‘n wettige permit moet verkry om in Suid-Afrika woonagtig te wees. Aangesien die koop of huur egter reeds gefinaliseer is, sal dit geen impak hê op die geldigheid van die voltooide koop of verhuring nie.

Ter samevatting, ‘n buitelander wat buite die grense van Suid-Afrika woonagtig is, mag eiendom in Suid-Afrika huur of koop. Die beperkings rakende plaaslike finansiering, veral waar die verkryging van finansiering `n opskortende voorwaarde van die ooreenkoms is, asook die vereistes vir ondertekening van dokumentasie in die buiteland, moet in gedagte gehou word aangesien dit tydrowend kan wees en addisionele kostes kan meebring voordat die eiendom registreer kan word.

A ‘rouwkoop’ clause included in a sale agreement provides for the purchaser to pay a deposit to the seller, which deposit may be retained by the seller should the purchaser decide to withdraw from the agreement. This does not constitute breach of the agreement, but is a mechanism whereby the purchaser legally buys his way out of the agreement.

Most sale agreements providing for the payment of a deposit, also contain a provision that this deposit will be forfeited should the purchaser breach the agreement. The Conventional Penalties Act of 1962 does however provide the purchaser with a remedy if the penalty exceeds the damages, as a Court may be approached for a refund of the difference between the penalty amount and the amount of the actual damages suffered.

The inclusion of either a penalty clause or a ‘rouwkoop’ clause in the sale agreement are effective methods for the seller to ensure that he is dealing with a serious purchaser.

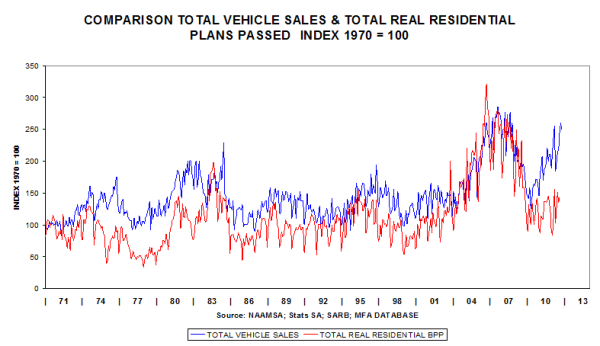

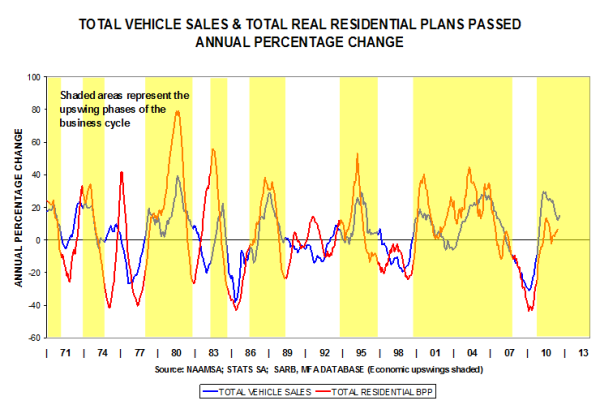

Vehicle Sales & Transfer Duty November 2011.

Total vehicle sales were 19% higher in Oct 2011, compared to Oct 2010. Compared to Sep 2011, they were 4% lower.

The (smoothed) annual percentage change of vehicle sales is currently 15%, and is a mirror image of plans passed, albeit on a higher plane.

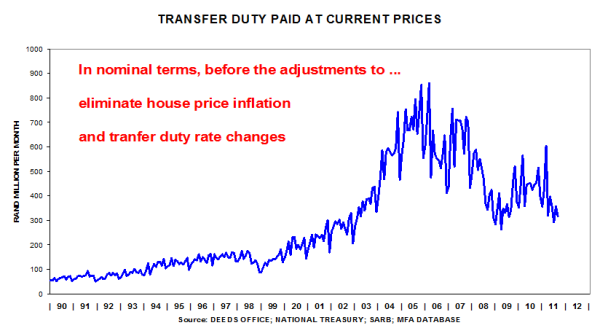

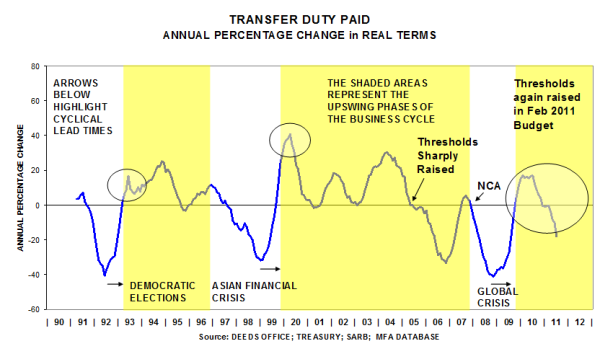

The poor state of the residential property market is reflected in poor nominal levels of transfer duty gathered by the fiscus

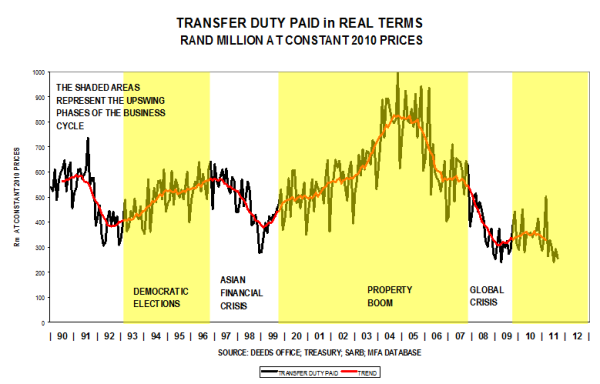

In real terms the lacklustre performance is just as evident. Real levels are now on a par with those prevailing during the 2008/09 financial Crisis.

When analysing year-on-year changes, the cyclical pattern is evident, except that the percentage movement is currently negative, compared with smaller positive movements in 1993 and in 2000 (refer circles). More evidence of extreme weakness in the residential property market. In fact, the percentage decline is severe, at -18%.

Mandate agreements need to comply with the requirements of the CPA in the following respects:

- Mandate agreements must be drafted in plain and understandable language (the plain language provisions In the Act). It is advisable to have mandate agreements available in a language which is best understood by a consumer. For example, in Kwa-Zulu Natal mandate agreements should also be available in isi-Zulu, and in the Western Cape, Afrikaans;

- Mandate agreements must not contain terms that are unnecessarily onerous on the seller - the court or the Consumer Tribunal will have the power to vary or strike out terms that are unfair, unreasonable or unjust and agents may find it difficult to claim commission based on such mandates, or may find their commission reduced by the court or Consumer Tribunal;

- In terms of the Act, agreements must be interpreted to the benefit of the consumer, especially where an agreement contains an ambiguity, restriction or limitation and estate agents can no longer rely on the onerous conditions contained in their existing mandates. Agents may find that the courts will make a value judgment and not uphold or enforce commission claims where such claim is based on mandate agreements which contain wording that can be regarded as unconscionable or unfair, or where a consumer (seller) did not fully understand the meaning of a mandate agreement signed by him.

To get a copy of the mandate please contact the author.

An onerous title deed condition that isn’t discovered in time could delay or prevent the progress of a property development – with serious cost implications. Alternatively, such an omission could be costly when buying or selling property.

Given this truism, the purpose of this article is to sensitise the reader to some pitfalls when dealing with title deeds.

The deeds registration offices had a system whereby deeds were lodged in duplicate and the Deeds Office would endorse changes of ownership, caveats, interdicts, mortgage bonds, and servitudes against the title deeds. They would keep one copy for records purposes and the other copy would be given back to the client.

It was not practice, nor prescribed in any Act, that conditions be carried forward from deed to deed. In the Deeds Registries in the former Cape Province the so-called pivot deed system had existed prior to 1937. The pivot deed system is unique to the Cape Town deeds registry. In terms of this system, no conditions were carried forward in a title deed. The title deed conditions would simply state:

“Subject to the conditions as contained in Deed of Transfer No … [with reference to the prior

title deed]”.

When searching the above pivot deed, one would find that these deeds in turn make reference to earlier title deeds.

It is only since 1937 that title deed conditions have been carried forward in each new title deed. Thus, to determine all the possible conditions against and in favour of a property, proper research must be done and all previous title deeds must be checked, from the day when the first Government Grant or Crown Grant was issued up to 1937.

The practical way would be to employ a conveyancing attorney, skilled in these matters, to conduct the research and prepare a Conveyancer’s Certificate to certify that

* the Conveyancer did a search behind the pivot deed and

* found no onerous conditions relevant to the proposed nature of the transaction or development, etc.

Developments since the 1980s

The Deeds Registration offices introduced a micro filming system, and since then all title deeds lodged are microfilmed. In addition, a scanning system was introduced in 2007/ 2008. Thus, Deeds Office records are now kept on both microfilm and in digital format, while the original title deeds are sent back to the attorneys for delivery to the new owner or bank(s). Title deeds are endorsed with changes in ownership, mortgage bonds and all other propertyrelated transactions. This of course depends on the instruction the deeds office had received on lodgement from the conveyancing firm.

The Deeds Offices continually update their records and one can obtain a “Deeds Office printout” to view the most current information listed against the property, viz.:

- Interdicts and caveats (examples are court orders, insolvency and rehabilitation notices, sequestration orders, liquidation orders, notices from the Surveyor General’s office, and expropriation notices).

- Sectional title information, such as

- Exclusive use areas.

- Rights of further extension reserved by the developer (section 25).

- Servitudes on common property.

- Notarial servitudes

- Mortgage bonds

It is, however, also important to note that updated information pertaining to property transactions can take, from date of registration, as long as 5-8 working days to appear on the system of the Deeds Offices. Sectional-title transactions can take up to 10 days and other transactions that involve cross-writing in title deeds filed in counter cover can take up to three weeks.

(Cross-writing is the updating of all relevant and related information in documents filed at Deeds Registration offices. The counter-cover system applies where 20 or more properties are held under one title deed, and where the client requests the Deeds Office to keep the original title deed in its records.)

Some advice

In sum, to protect one’s interests, it is a good idea to appoint a conveyancing attorney to conduct a search at the Deeds Office and peruse or verify the following information that might be applicable to the subject property:

- Conditions in the current title deed

- Conditions behind the pivot deed

- Information on the Deeds Office printouts, such as:

- Caveats.

Servitudes.

Interdicts.

And, lastly, if you are a developer, remember to appoint a town planner to assist with the restrictions imposed by the local authority and, if applicable, zoning requirements.